AI in Insurance: Innovating Without Losing Control

Artificial intelligence is already reshaping insurance. It is changing how risk is assessed, how claims are handled, and how insurers engage with customers. But as AI adoption accelerates, one question matters more than ever: how do insurers innovate quickly without losing control, governance, or trust?

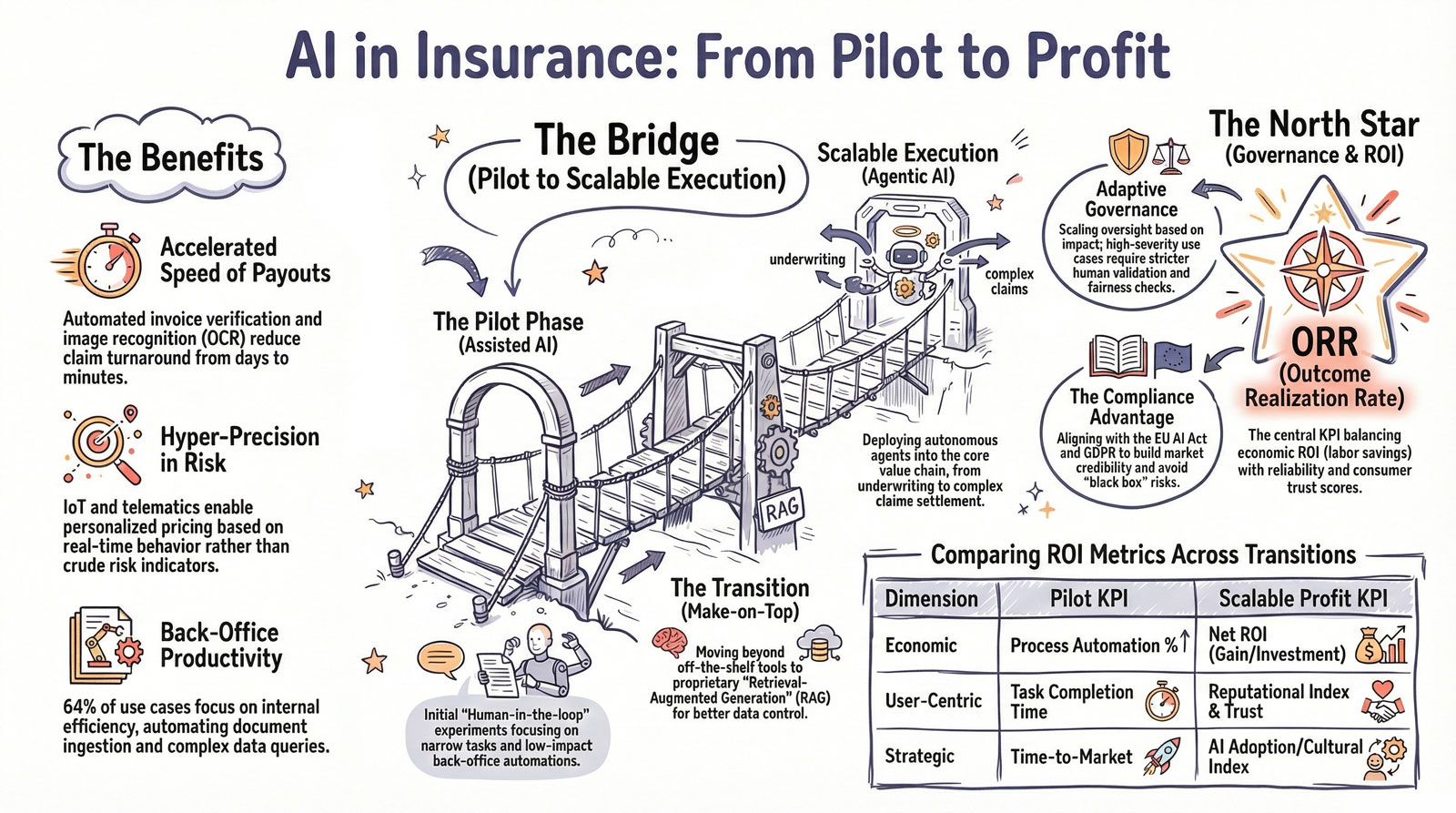

For Etiqa, innovation only matters when it delivers measurable outcomes. In insurance, that means applying AI in ways that improve speed and performance while keeping data secure, decisions auditable, and governance clear. The goal is not to deploy more tools for the sake of it. The goal is to turn innovation into real-world value, with accountability built in from the start.

From Reactive to Predictive Insurance

The biggest shift AI brings to insurance is a move away from a purely reactive model. Traditionally, insurers respond after a loss occurs. AI makes it possible to become more proactive and predictive, using data to anticipate risk and improve decisions before issues escalate.

This is already visible in three critical areas:

- Pricing and underwriting, with more granular risk assessment

- Claims management, with faster and more automated workflows

- Fraud detection, through pattern recognition and anomaly monitoring

With telematics, IoT, and predictive models, premiums can better reflect actual customer behavior. With computer vision, damage assessments can move from days to minutes. With machine learning applied to historical and real-time data, suspicious claims can be identified earlier, reducing both fraud losses and operational inefficiency.

The Real Challenge: Data Control and Lock-In Risk

The value of AI in insurance is clear. The risks are just as clear. Insurance organizations work with sensitive data, highly regulated processes, and decisions that directly affect people and businesses. That makes architecture as important as the models themselves.

A strong enterprise approach combines:

- Retrieval-Augmented Generation (RAG), to use current business data without permanently absorbing proprietary information into models

- Model Context Protocol (MCP), to securely connect AI models with enterprise systems and datasets

- Audit trails and logging, to make AI actions traceable and reviewable

- Multi-cloud and multi-model strategies, to reduce dependence on a single provider

In practice, insurers do not just need AI. They need AI that works with the right data, under the right permissions, and with a record of every meaningful action.

That means designing systems with:

- rigorous authentication and authorization

- encryption in transit and at rest

- isolation for highly sensitive information

- clear exit paths to reduce vendor lock-in

For Etiqa, this is where the brand promise becomes practical: innovation should serve goals, not create new forms of dependency.

Governance Still Belongs to People

Automation is often the headline in AI discussions. In insurance, however, accountability remains human.

AI can support faster, better-informed decisions, but it cannot become an opaque black box. Governance must make sure technology remains understandable, reviewable, and aligned with customer trust.

That requires:

- Human-in-the-loop oversight, where trained teams can review, reject, or override AI outputs

- Transparency for customers, where required by applicable law, especially when people are directly interacting with certain AI systems

- Risk assessments, including bias, error, and potential impact on fundamental rights

- Compliance controls, aligned with GDPR, the EU AI Act, and supervisory expectations

Under the EU AI Act, certain AI systems used for risk assessment and pricing for natural persons in relation to life and health insurance are explicitly classified as high-risk use cases. For certain deployers of high-risk AI systems, the AI Act may also require a Fundamental Rights Impact Assessment before the system is put into use, depending on the specific role and use case.

For Etiqa, governance is not a constraint on innovation. It is what makes innovation sustainable.

What the Next Few Years Will Change

The insurance sector is now entering a new phase of AI maturity. Three developments will shape the next wave.

1. More Operational Automation

AI will increasingly move from decision support into workflow execution. In many cases, systems will be able to:

- intake claims

- classify documents

- generate operational recommendations

- support low-complexity case handling

This agentic shift creates significant upside, but only if orchestration and controls are strong enough to manage it.

2. More Pressure on Explainability and Security

As adoption grows, so will scrutiny around:

- model hallucinations

- prompt injection

- data quality

- system resilience

In insurance, these are not secondary technical concerns. They affect reputation, business continuity, customer fairness, and regulatory compliance.

3. More Need for Hybrid Models

The most effective insurers are unlikely to rely on a single AI approach. A pragmatic model will combine:

- generative AI for unstructured data such as documents, emails, and reports

- traditional machine learning for pricing, scoring, and predictive decisions

- controlled environments for the most strategic or sensitive data

- external APIs for lower-risk, generic use cases

This hybrid model reflects Etiqa’s broader capability approach: use the right technology for the right outcome, with clear ownership and guardrails.

The Business Opportunity

When implemented well, AI can help insurers achieve measurable improvements such as:

- reduced claims processing time

- more accurate risk assessment

- higher back-office productivity

- stronger fraud prevention

- more personalized products and services

- better customer experience

But technology alone does not create return on investment. Results depend on turning pilots into scalable execution, with clear ownership, transparent reporting, and confidence that spending is tied to outcomes.

This is where Etiqa’s North Star matters. Outcome Realization Rate (ORR) is the guiding principle behind how innovation should be measured: initiatives should achieve predefined business outcomes within target timeframes and with governance that stakeholders can trust.

Conclusion

Artificial intelligence will continue to transform insurance. The insurers that lead will not simply be the ones that deploy the most AI. They will be the ones that integrate it with discipline.

The future belongs to organizations that can balance four priorities at once:

- innovation

- data control

- governance

- customer trust

AI can make insurance faster, more accurate, and more responsive to real needs. But only when it is designed responsibly and connected to outcomes that matter.

For Etiqa, that is the standard: innovation should deliver measurable value, with guardrails always in place.

Latest articles

Interview with Giacomo Gorgellino - Etiqa's Senior DevOps Engineer

Read more.png)

Inside Multiply Labs - CEO Fred Parietti's visionary journey in Robotics and Pharma

Read more.png)

Interview with Michele Roberti - Etiqa's Full Stack Developer

Read more